AdaptiveMeanReversionBot · Regime-adaptive — strategy & live paper-trading performance

AdaptiveMeanReversionBot is a production algorithmic trading strategy paper-traded live from a $10,000 seed. Live paper-trading performance: 73.32% …

Read Article

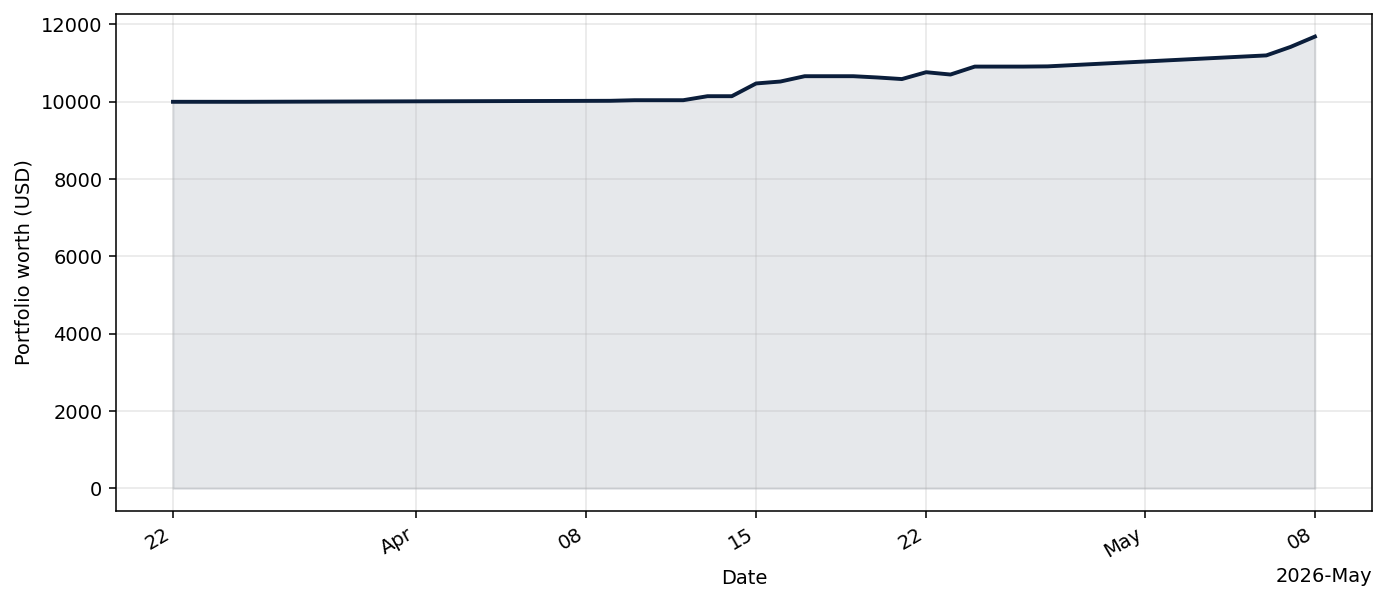

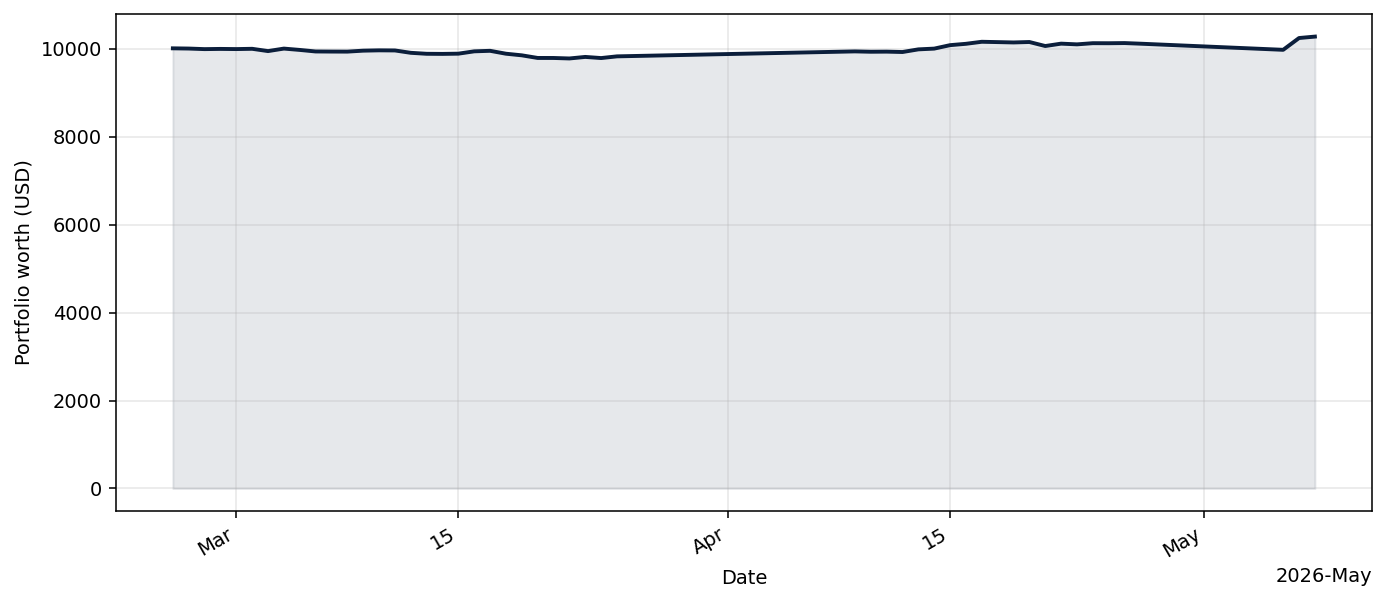

RegimeAdaptiveBot is a production algorithmic trading strategy paper-traded live from a $10,000 seed. Live paper-trading performance: 7.19% annualised return (2.50% total), Sharpe 0.85 over 109 days.

tradingbot/regimeadaptivebot.py.See the full chart, current holdings, and historical backtest on the strategy’s live page →.

A full technical writeup for RegimeAdaptiveBot is in progress. In the meantime:

tradingbot/regimeadaptivebot.py.RegimeAdaptiveBot is part of the open-source python_tradingbot_framework — fork the repo, run the code locally, or deploy your own variant. The source lives at tradingbot/regimeadaptivebot.py. The live page shows today’s portfolio state alongside the full historical backtest.

Since deployment, RegimeAdaptiveBot has produced an annualised return (CAGR) of 7.19% on a $10,000 paper seed (2.50% cumulative), with a Sharpe ratio of 0.85 and a max drawdown of -2.34% over 109 trading days. Numbers refresh daily on the live page.

Yes. RegimeAdaptiveBot is part of the open-source python_tradingbot_framework — you can fork the repo, inspect the strategy, and run the code locally or on your own Kubernetes cluster. The exact source file is here.

RegimeAdaptiveBot belongs to the Regime-adaptive family. Detects market regimes (trend vs. mean-reversion) and switches strategy per regime. Browse the full leaderboard to compare it against strategies from other families.

Browse the full live leaderboard to see how RegimeAdaptiveBot ranks against 23 other paper-traded strategies, all seeded with the same $10,000.

AdaptiveMeanReversionBot is a production algorithmic trading strategy paper-traded live from a $10,000 seed. Live paper-trading performance: 73.32% …

Read ArticleResearch portal. Not investment advice and not a solicitation. Strategies shown are paper-traded with a $10,000 simulated seed; no real client …

Read Article