-60% p.a.

bt_headshoulder_sharpeopt_mixed

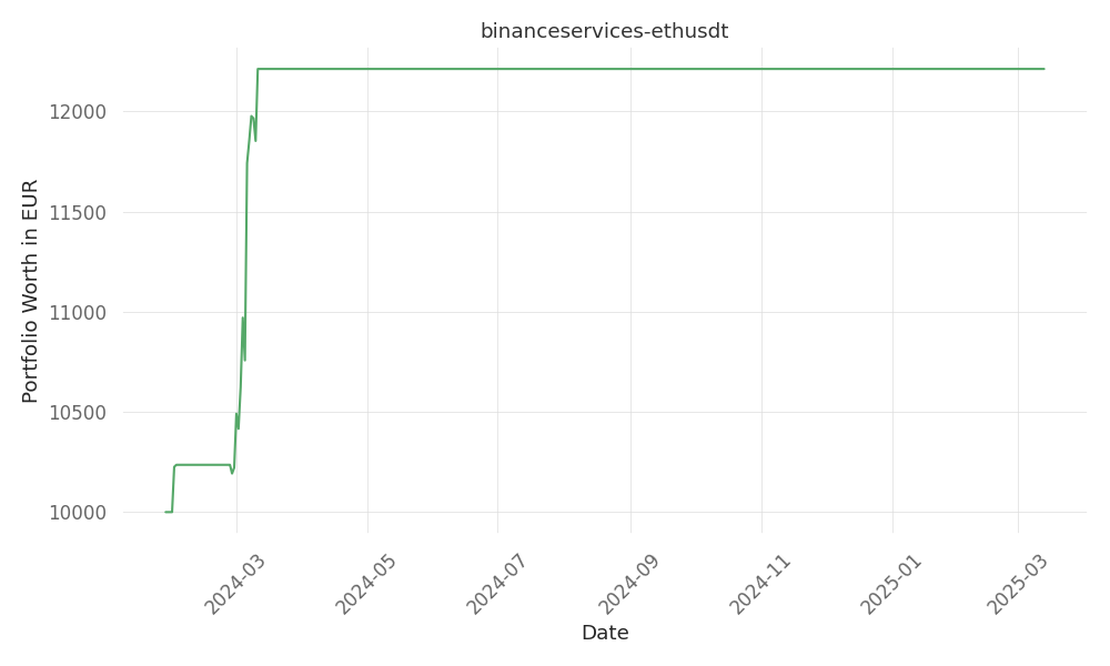

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. -60 Days active 408 …

tickers: AVGO

source: Benzinga

| ticker | polarity | why? |

|---|---|---|

| AVGO | positively | The ticker AVGO (Broadcom, Inc.) will be affected positively by the continued strong performance in the AI market, adding several new AI customers and the growing demand for its products and services. As analysts believe the company’s forecasts are too conservative, the market’s outlook for AVGO look positive and the stock could potentially rally further. Another factor is the sturdy relations > |

| with its dealings being done in house giving it more power over its buyers which will eventually lead to their dependence on it. |

static-skfolio-nested-cluster-optimization , static-skfolio-max-sortino , newstrader , bt_headshoulder_sharpeopt_mixed

March 7, 2025 Broadcom, Inc. has outperformed expectations for both the quarter just concluded and the quarter to come according to multiple analysts. This news comes as broadcom continues its upward trend in the AI market, adding several new AI customers. Regarding the company’s forecasts, we deemed them too conservative. Adding it all up, it is clear that Broadcom is well-positioned. Bullish Bent And since the markets dove in the second half of last year, stock prices have not been driven high enough. Several customers cited by analysts range from AI-related, such as ARM, OpenAI, and even to Apple. Anyone with a consumer tech product and who is a USP (Ultimate Software Product) wants to design with it, figure out the fabrication, fusion, or all types, get the job done, and Broadcom has it. Add it all up, the consensus on AVGO is Beilde But en route to realizing that apparently modest call on. The 77% jump in year-over-year artificial growth numbers is a dramatic top line increase, and benchmark capitalizes, amplifying its growth. At 17.9X 2025 EPS, CRM is an ROI dispute on lead outcome here in case someone didn’t pay attention - their turnover is dramatic. Key here is no one else is even in the same ballpark, knowing no one else takes the risk on Multi-billion-dollar overlays, dives up front for sales ramps down the line. The relationships are sold CASP’s way - doing everything in house. Which gives power where a buyer has no way to get to the next step without CRM and will ultimately do anything CRM asks. Conclusion Broadcom is no cheap stock, but it’s a growth play which has seen its days of fast growth come and go. It has at this point. By leveraging this reality for the next several years we see AVGO as an overbought growth play currently.

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. -60 Days active 408 …

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. -85 Days active 427 …

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. 19 Days active 410 …