-60% p.a.

bt_headshoulder_sharpeopt_mixed

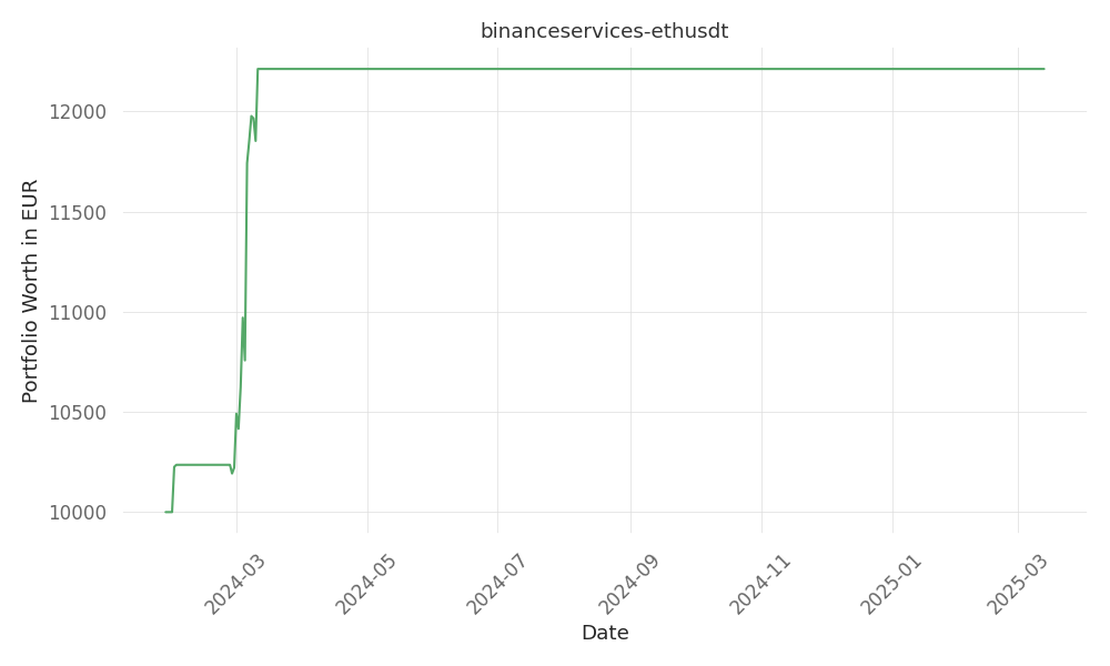

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. -60 Days active 408 …

tickers: NVDA

source: Motley Fool

| ticker | polarity | why? |

|---|---|---|

| NVDA | positively | Investors should note that NVDA, after reporting Q4 earnings, is still a top performer for 2024, based on the impressive growth numbers of 171%. Despite some losses in the past year, continuing to grow the data center segment as well as expanding focuses in automotive and robotics will keep interest in NPDA high. This could drive future interest buy patterns. |

c-bigtech-momentum , randombot , static-skfolio-denoised-cov-shrunk-expret , finnhub-recommendations , bt_headshoulder_sharpeopt_mixed , newstrader , xgb_sharpeopt_trenddet , static-skfolio-max-sortino

One of the most highly anticipated quarterly reports on Wall Street was delivered by Nvidia (NASDAQ: NVDA) last night, and the artificial intelligence (AI) powerhouse didn’t disappoint. Data center revenue continued its upward trajectory, and CEO Jensen Huang remained as optimistic as ever. Despite the impressive performance, Nvidia’s stock saw declines of as much as 5% today. By 11:45 a.m. ET, shares were still down by 3.5%, extending its losses this year after an extraordinary 171% return in 2024. Despite the stock’s decline, the current state of the business might present a valuable opportunity for long-term investors. The company had previously guided investors to expect revenue of approximately $37.5 billion in the fourth quarter. True to its track record, Nvidia exceeded this projection with sales of $39.3 billion. The full-year revenue more than doubled year over year, showcasing the company’s robust growth trajectory. Investors are now looking ahead to assess when this growth might slow. Nvidia anticipates sales of about $43 billion in the current quarter, indicating a sequential growth rate of less than 10% compared to the mid-teens growth rate seen throughout most of 2024. During the investor conference call, CEO Jensen Huang mentioned, “Data center sales in China remained well below levels seen on the onset of export controls. The market in China for data center solutions remains very competitive.” Additionally, there are concerns about a decline in profitability. Gross margins in the current fiscal first quarter are expected to be about 71%, compared to 75% in the fiscal year ended Jan. 26. While Nvidia continues to show significant growth and profitability in the data center business, another growing segment is its automotive and robotics division. This segment has demonstrated impressive quarterly growth. Although it trails data center AI sales, it is poised to drive Nvidia’s next phase of growth.

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. -60 Days active 408 …

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. 19 Days active 410 …

Introduction to our strategy no description yet Quick Summary Metric Value Return % p.a. -85 Days active 427 …