Investment thesis

Regime-adaptive — economic intuition. Financial time series alternate between trending and mean-reverting regimes. A single static strategy is structurally mis-specified in at least one regime. This family detects the regime and switches logic, monetising regime-transition risk that pure trend or pure mean-reversion books leave on the table.

Risk-adjusted performance — live track record

Forward-tested daily against live market data. Metrics derived from end-of-day portfolio marks; methodology documented on the Due Diligence and About pages.

| Return | Value | Risk-adjusted | Value | |

|---|---|---|---|---|

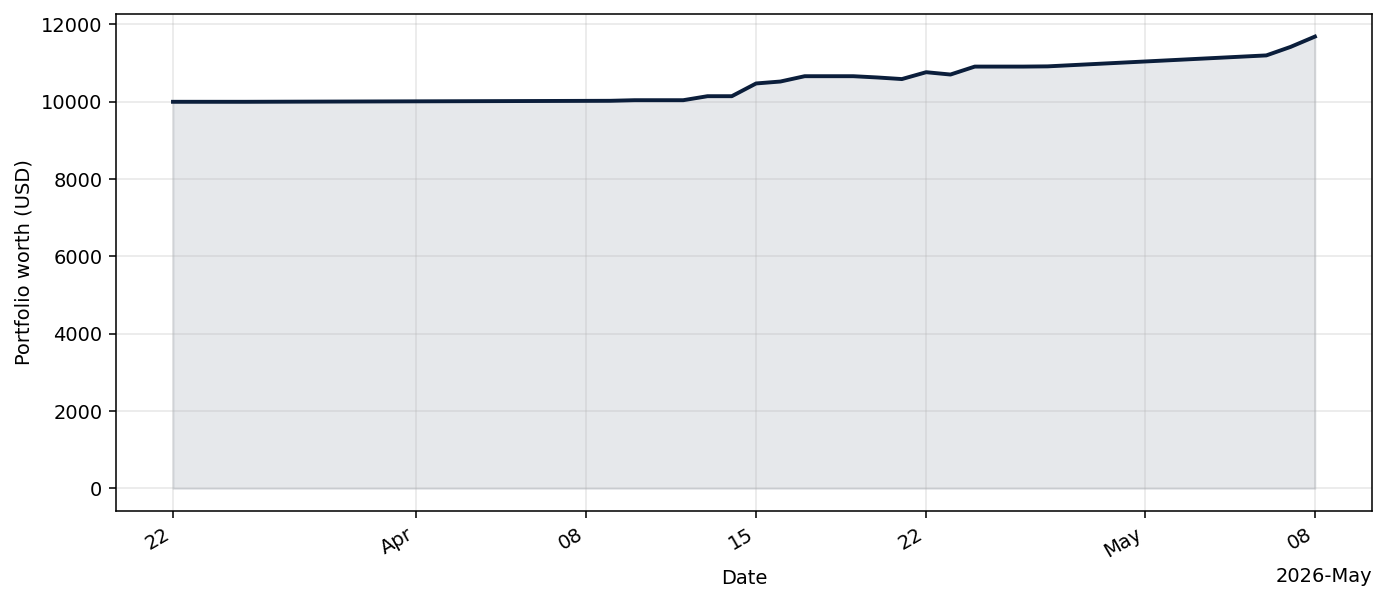

| Current portfolio worth | $11712.87 | Sharpe ratio | 2.44 | |

| Total return | 17.13% | Sortino ratio | 2.77 | |

| CAGR | 73.32% | Calmar ratio | 10.43 | |

| Volatility (annualised) | 20.51% | Profit factor | 1.66 | |

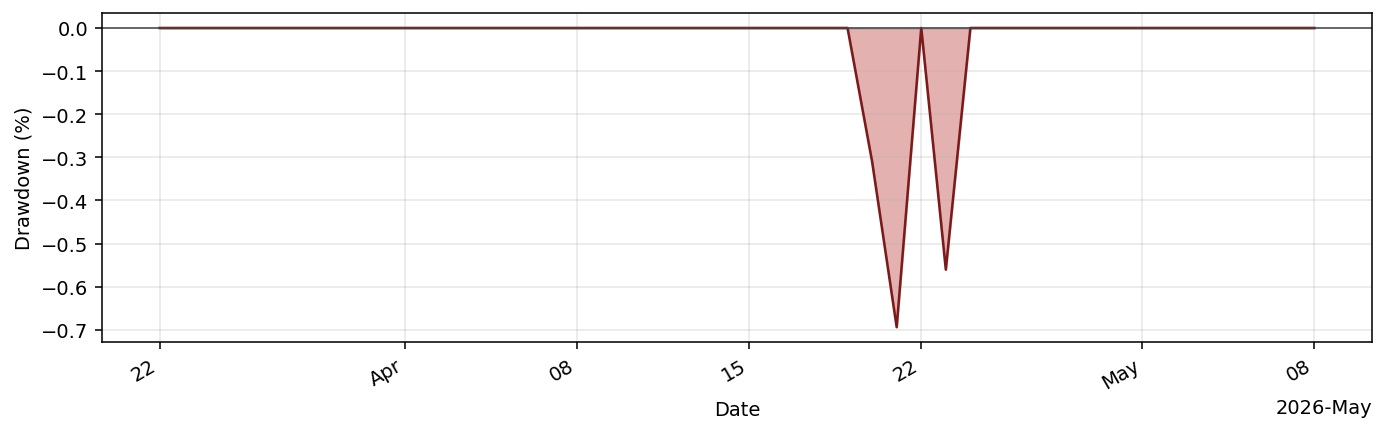

| Days live | 84 | Maximum drawdown | -7.03% |

Process consistency

| Positive months | 50.0% |

| Best month | 11.13% |

| Worst month | -3.13% |

| Recovery from max drawdown | still underwater |

Market independence

Correlation and beta versus passive benchmarks, computed over the full live series.

| Benchmark | Correlation | 90-day rolling correlation | Beta |

|---|---|---|---|

| S&P 500 (SPY) | 0.86 | 0.00 | 1.58 |

| Bitcoin (BTC-USD) | 0.21 | 0.00 | 0.13 |

A correlation materially below 1.0 to both benchmarks indicates the strategy’s returns are not a simple re-expression of long equity or long crypto beta.

Equity curve

Live track record — forward-tested performance from the strategy's production start date.

Drawdown profile

Underwater curve — percentage below the running high-water mark. Institutional allocators read this before the equity curve.

Current holdings

| Symbol | Quantity |

|---|---|

| QQQ | 16.4336 |

| USD | 0.0000 |

Research & documentation

- Strategy deep-dive: AdaptiveMeanReversionBot: strategy deep-dive & live performance

- Methodology write-up: AdaptiveMeanReversionBot

- Reference implementation:

tradingbot/adaptivemeanreversionbot.py - Framework: python_tradingbot_framework (open source, fully inspectable)

Related strategies

Other strategies in the Regime-adaptive family:

- RegimeAdaptiveBot · research note- TARegimeAdaptiveBot · research note Or view the full strategy roster.

For professional investors

Request the investor deck, DDQ, and extended analytics. Firm-gated and reviewed manually.

Request access