Investment thesis

Portfolio optimisation — economic intuition. Given a universe of imperfectly-correlated return streams, convex optimisation (Markowitz, risk-parity, recursive decay) produces weights that dominate naive equal-weight on a risk-adjusted basis. The edge is not in alpha discovery but in the disciplined combination of existing signals — consistent with institutional multi-manager allocation.

Risk-adjusted performance — live track record

Forward-tested daily against live market data. Metrics derived from end-of-day portfolio marks; methodology documented on the Due Diligence and About pages.

| Return | Value | Risk-adjusted | Value | |

|---|---|---|---|---|

| Current portfolio worth | $10128.53 | Sharpe ratio | 0.34 | |

| Total return | 1.29% | Sortino ratio | 0.50 | |

| CAGR | 2.29% | Calmar ratio | 0.34 | |

| Volatility (annualised) | 7.71% | Profit factor | 1.08 | |

| Days live | 139 | Maximum drawdown | -6.76% |

Process consistency

| Positive months | 71.4% |

| Best month | 4.24% |

| Worst month | -5.33% |

| Recovery from max drawdown | 27 days |

Market independence

Correlation and beta versus passive benchmarks, computed over the full live series.

| Benchmark | Correlation | 90-day rolling correlation | Beta |

|---|---|---|---|

| S&P 500 (SPY) | 0.51 | 0.00 | 0.38 |

| Bitcoin (BTC-USD) | 0.24 | 0.19 | 0.06 |

A correlation materially below 1.0 to both benchmarks indicates the strategy’s returns are not a simple re-expression of long equity or long crypto beta.

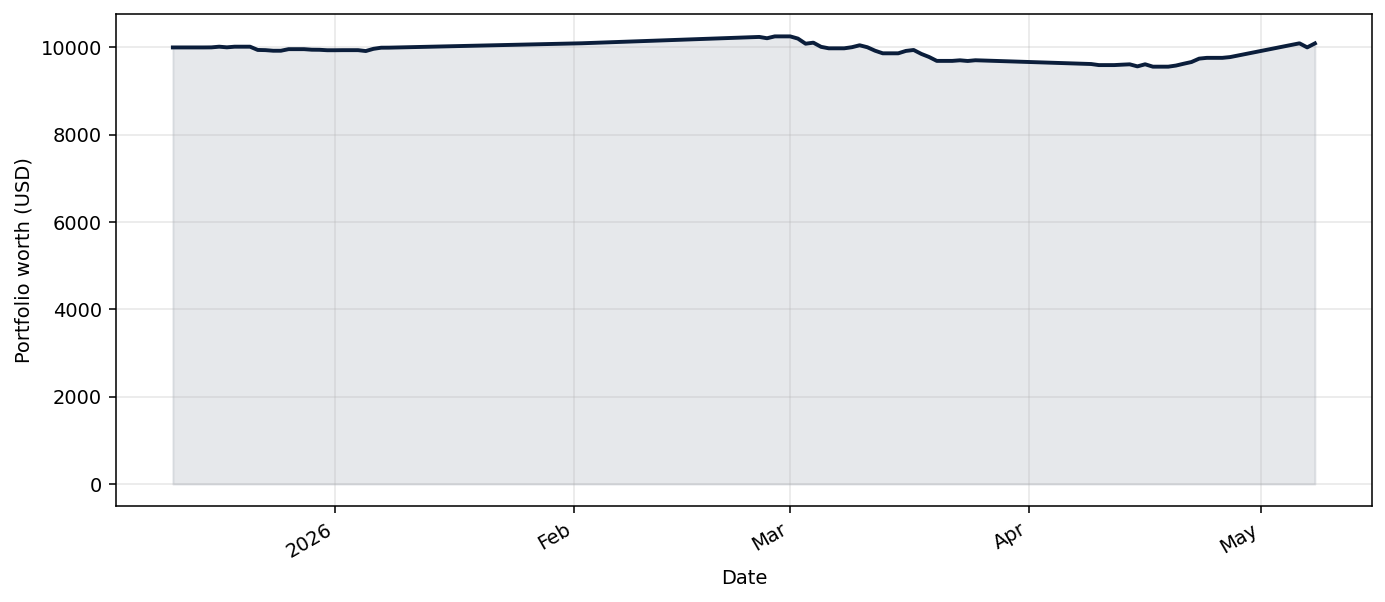

Equity curve

Live track record — forward-tested performance from the strategy's production start date.

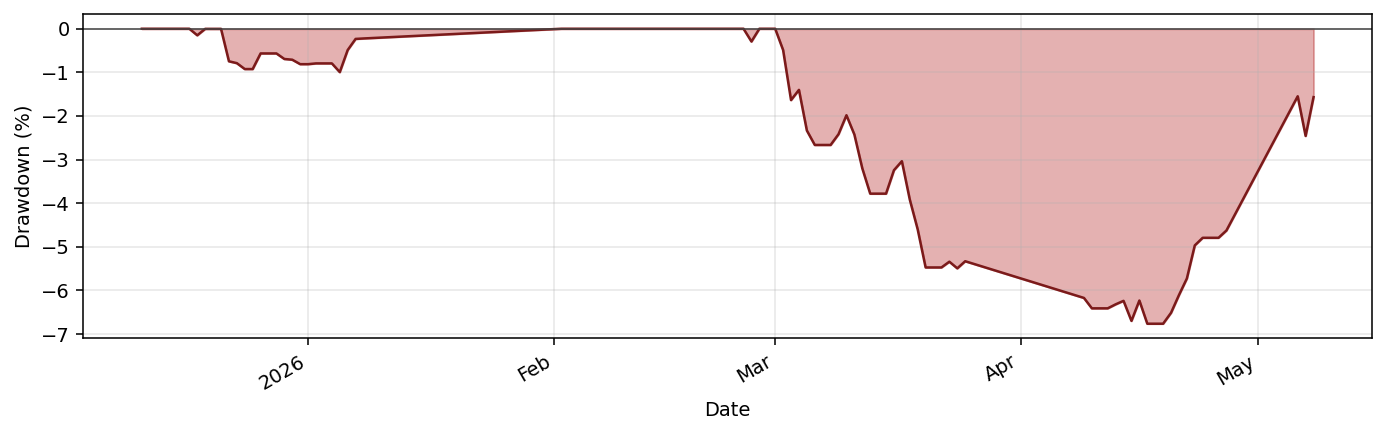

Drawdown profile

Underwater curve — percentage below the running high-water mark. Institutional allocators read this before the equity curve.

Current holdings

| Symbol | Quantity |

|---|---|

| 2B76.DE | 6.5355 |

| AMD | 0.4323 |

| BTEC.L | 38.1712 |

| DBMF | 27.9082 |

| GOOG | 0.2631 |

| IWDA.AS | 4.2583 |

| KDP | 5.7365 |

| L0CK.DE | 8.2767 |

| LLY | 0.1213 |

| META | 0.2732 |

| NTSX | 7.6706 |

| PGR | 1.6298 |

| QQQ | 0.5239 |

| SHV | 18.3598 |

| SQQQ | 11.7100 |

| TEAM | 0.0000 |

| UNH | 0.6366 |

| UPRO | 1.0874 |

| USD | 0.0000 |

| UUP | 71.2639 |

| VFH | 4.6271 |

| VLUE | 1.9607 |

| W1TA.DE | 1.4250 |

| XAIX.DE | 0.6636 |

Research & documentation

- Strategy deep-dive: SharpePortfolioOptWeeklyBot: strategy deep-dive & live performance

- Reference implementation:

tradingbot/sharpeportfoliooptweekly.py - Framework: python_tradingbot_framework (open source, fully inspectable)

Related strategies

Other strategies in the Portfolio optimisation family:

- RecursiveDecayHarvestBot · research note- SynthesizedHyperConvexityBot · research note Or view the full strategy roster.

For professional investors

Request the investor deck, DDQ, and extended analytics. Firm-gated and reviewed manually.

Request access